Introduction

Finance workflow automation is no longer a back-office efficiency project. For CFOs and finance operations leaders, it is a strategic lever that directly impacts reporting accuracy, cash flow visibility, audit compliance, and the capacity of finance teams to support business decisions rather than manage transactions.

The opportunity is well-documented: finance functions that operate with manual or semi-manual workflows spend 60–70% of their team’s capacity on transaction processing. That capacity should be directed toward analysis, forecasting, and strategic partnership with the business. Automation is not about reducing headcount—it is about redirecting it.

This playbook maps the core finance workflow automation use cases, the architecture required for each, and the ROI framework that supports CFO-level investment decisions. It is designed to help finance leaders move from a conceptual understanding of automation potential to a deployment-ready programme design.

The Four Core Finance Workflow Automation Use Cases

1. Budget Approval Automation

Budget approval processes in most enterprises are among the most fragmented workflows in the organisation. Annual budget cycles, quarterly reforecasts, and ad hoc budget requests generate hundreds of approval tasks that travel through email chains, shared spreadsheets, and informal channels—creating version control nightmares and audit gaps.

Finance workflow automation for budget approvals creates a structured, governed process:

- Budget requests are submitted through a structured form that captures request type, cost centre, amount, business justification, and GL account

- Approval routing is driven by the request type and amount, with automatic routing to cost centre owner, finance business partner, and CFO office as required by policy

- Approval decisions are recorded in the audit trail with full metadata

- Approved budgets are written to the planning system or ERP budget module automatically

The governance benefit extends beyond efficiency: a properly automated budget approval workflow provides finance with real-time visibility into approved commitments, pending requests, and budget utilisation—replacing the spreadsheet-based tracking that creates reporting lag.

2. Vendor Payment Workflow Automation

Vendor payment workflows span procurement and finance, and their failure modes are costly: late payment penalties, early payment discount misses, and vendor relationship damage from inconsistent payment communication.

The payment workflow connects to the accounts payable process described in our guide on accounts payable automation from invoice to payment. From the finance workflow perspective, the key automation requirements are:

- Automated payment term tracking: identifying invoices eligible for early payment discounts and prioritising their processing

- Payment batch assembly: grouping approved invoices into payment batches based on payment method, currency, and entity

- Exception handling for payment holds: automating notifications when payments are placed on hold due to dispute or compliance review, and routing resolution to the appropriate owner

- Bank file generation: producing the payment instruction file for the banking interface from the approved payment batch, without manual file preparation

3. Expense Reimbursement Workflow Automation

Expense management is a high-volume, low-complexity process that is ideally suited to automation. The typical enterprise expense reimbursement workflow generates significant administrative overhead relative to the transaction values involved.

Automated expense workflows handle:

- Policy validation at submission: checking expense claims against company policy (meal limits, travel class, receipt requirements) and flagging violations before the approval step

- Receipt matching: AI-based receipt verification that matches submitted receipts against claimed amounts and dates

- Approval routing: routing to the direct manager for standard claims within policy; routing to finance for exception claims or high-value submissions

- ERP posting: posting approved expenses to the correct GL accounts and cost centres automatically upon approval

The policy validation step is where automation delivers the most governance value. Expense policy violations caught at submission—rather than during audit—prevent the awkward retroactive conversations that damage team relationships and generate correction rework.

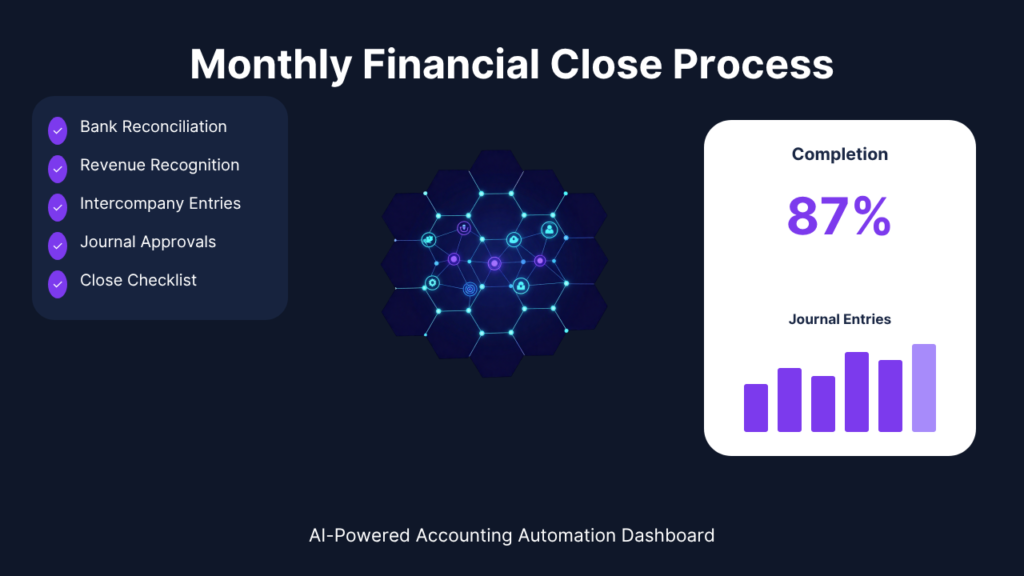

4. Financial Close Workflow Automation

The monthly financial close process is one of the most complex, time-sensitive workflows in the finance function. It involves dozens of discrete tasks—journal entry preparation, account reconciliation, intercompany eliminations, consolidation uploads—that must be executed in a defined sequence within a tight timeframe.

Financial close workflow automation addresses:

- Task sequencing and dependency management: Defining which close tasks must complete before others can begin, and automatically releasing downstream tasks when dependencies are met

- Preparer and reviewer assignment: Routing each close task to the assigned preparer, and automatically routing the completed task to the reviewer upon submission

- Status visibility: Real-time close progress dashboards showing task completion status, outstanding items, and projected close completion time

- Exception escalation: Automatic escalation of outstanding tasks that risk delaying the close, with defined escalation paths by task type and entity

Snoh Flow maps across these financial close workflows—budget approvals, vendor payments, expense reimbursements, and close management—with role-based visibility that gives CFOs and finance controllers a real-time view of process status across all open items.

The ROI Framework for Finance Workflow Automation

CFO-level investment decisions require a structured ROI framework. Finance workflow automation ROI has four components:

1. Processing cost reduction

Calculate the fully-loaded cost per transaction for each finance workflow (staff time + error correction + system overhead). Compare this to the automated processing cost. For AP workflows, industry benchmarks suggest a 65–80% reduction in per-invoice processing cost. For expense workflows, 50–65% reduction in per-claim cost. For budget approvals, the primary saving is in coordination overhead rather than direct processing cost.

2. Cycle time value

Shorter process cycle times have direct financial value. Earlier invoice processing captures more early payment discounts. Faster budget approvals reduce the delay between funding decisions and project execution. Faster close cycles compress the reporting lag between business events and management information availability. Quantify these values in terms of discount capture rates and decision latency costs.

3. Error and rework reduction

Manual finance workflows generate errors that require correction: duplicate payments, GL miscoding, unauthorised expense approvals. Rework costs are typically underestimated because they are distributed across AP analysts, finance business partners, and IT support. A systematic count of error-related rework hours over a quarter provides a credible baseline for quantifying this saving.

4. Compliance and audit cost reduction

Manual processes generate audit findings that require remediation. Automated workflows with full audit trails reduce both the frequency of findings and the cost of audit response. For public companies and regulated industries, the compliance value of automated workflow governance is often the most compelling element of the business case.

For a detailed ROI calculation framework applied to enterprise workflow automation, see our guide on how to measure workflow automation ROI for operations and finance teams.

Building the CFO’s Finance Automation Programme

A finance workflow automation programme should be sequenced to maximise early ROI while building the organisational capability required for more complex deployments.

Phase 1 — High volume, high friction: Start with the process that generates the most manual effort relative to transaction value. For most enterprises, this is accounts payable or expense reimbursement. Deploy automation on the standard path first; build exception workflows in Phase 2.

Phase 2 — Governance and compliance: Deploy audit trail, approval governance, and SLA management across all finance workflows. This phase converts automation efficiency into compliance readiness—a prerequisite for regulated industries and a value multiplier for all.

Phase 3 — Integrated financial close: Automate the close workflow after the foundational workflows are running reliably. Close automation depends on the data quality and process discipline established in Phases 1 and 2.

Phase 4 — Predictive and analytics layer: Deploy financial workflow analytics—cycle time trends, exception rate analysis, SLA performance, and predictive flagging. This layer is only valuable when Phases 1–3 generate sufficient process data to produce meaningful insights.

Conclusion

Finance workflow automation is a CFO-level strategic priority with measurable, quantifiable returns across four dimensions: processing cost, cycle time value, error reduction, and compliance. The practical starting point is sequencing automation by volume and friction—deploying on the standard path first, then building exception handling and governance infrastructure as the programme matures.

Three key takeaways:

- The ROI case for finance workflow automation is strongest when it combines processing cost reduction, cycle time value, and compliance assurance—not just headcount savings

- Financial close automation delivers the most governance value but depends on process discipline established in foundational AP and expense workflows first

- CFO sponsorship is the critical success factor—finance workflow automation that is owned by IT rather than finance typically fails to achieve the governance and analytics outcomes that justify the investment

The finance function has the most to gain from workflow automation. It also has the clearest line of sight to the financial value of investing in it.

FAQ

Which finance workflow should a CFO automate first?

Accounts payable is the most common starting point because it combines high transaction volume, clear ROI metrics (invoice processing cost and cycle time), and a well-understood automation architecture. The straight-through processing rate improvement from AP automation is also measurable within the first quarter of deployment, providing the data needed to build the internal case for Phase 2 investments.

How does finance workflow automation interact with existing ERP investments?

Finance workflow automation complements ERP systems rather than replacing them. The ERP is the system of record for financial data; the workflow platform manages the process that generates, validates, and approves that data before it enters the ERP. Integration is bidirectional: the workflow platform receives triggers from the ERP (new invoice, budget request submission) and writes outcomes back (approval status, GL coding, payment instruction). Well-designed integration does not require ERP customisation.

What governance controls should be in place before deploying finance workflow automation?

The foundational governance controls are: a current Delegation of Authority matrix defining approval authority by role and amount; documented exception handling procedures for the most common exception types; and defined audit trail retention and access requirements. Attempting to automate finance workflows without these governance foundations in place typically results in a high exception rate and workflow designs that require frequent reconfiguration as governance gaps are discovered in production.

How should finance leaders manage change resistance when deploying automation?

The most effective approach is to involve the finance team in process design before deployment. People who helped design the workflow are invested in its success. Framing automation as freeing the team from transaction work—rather than replacing it—addresses the most common concern. Early visible wins (reduction in overdue invoices, elimination of month-end close fire drills) build confidence and support for subsequent phases.

What data is needed to build a credible finance automation ROI business case?

At minimum: current transaction volumes (invoices per month, expense claims per month, budget requests per quarter), current average cycle times, current error rates and rework estimates, and current processing cost per transaction (staff time × hourly cost). Benchmark these against industry automation targets to size the potential saving. Add the discount capture opportunity (for AP) and audit cost reduction to complete the financial picture.